Growth Scare or Recession: What's Coming Next?

Recently, the stock market has experienced significant declines, with the S&P 500 and NASDAQ dropping over 5% and 8%, respectively, and major companies like Nvidia and Amazon seeing substantial drawdown. This downturn is largely due to three factors: tariffs, the Doge policy aimed at cutting government waste and national debt, and seasonal variations.

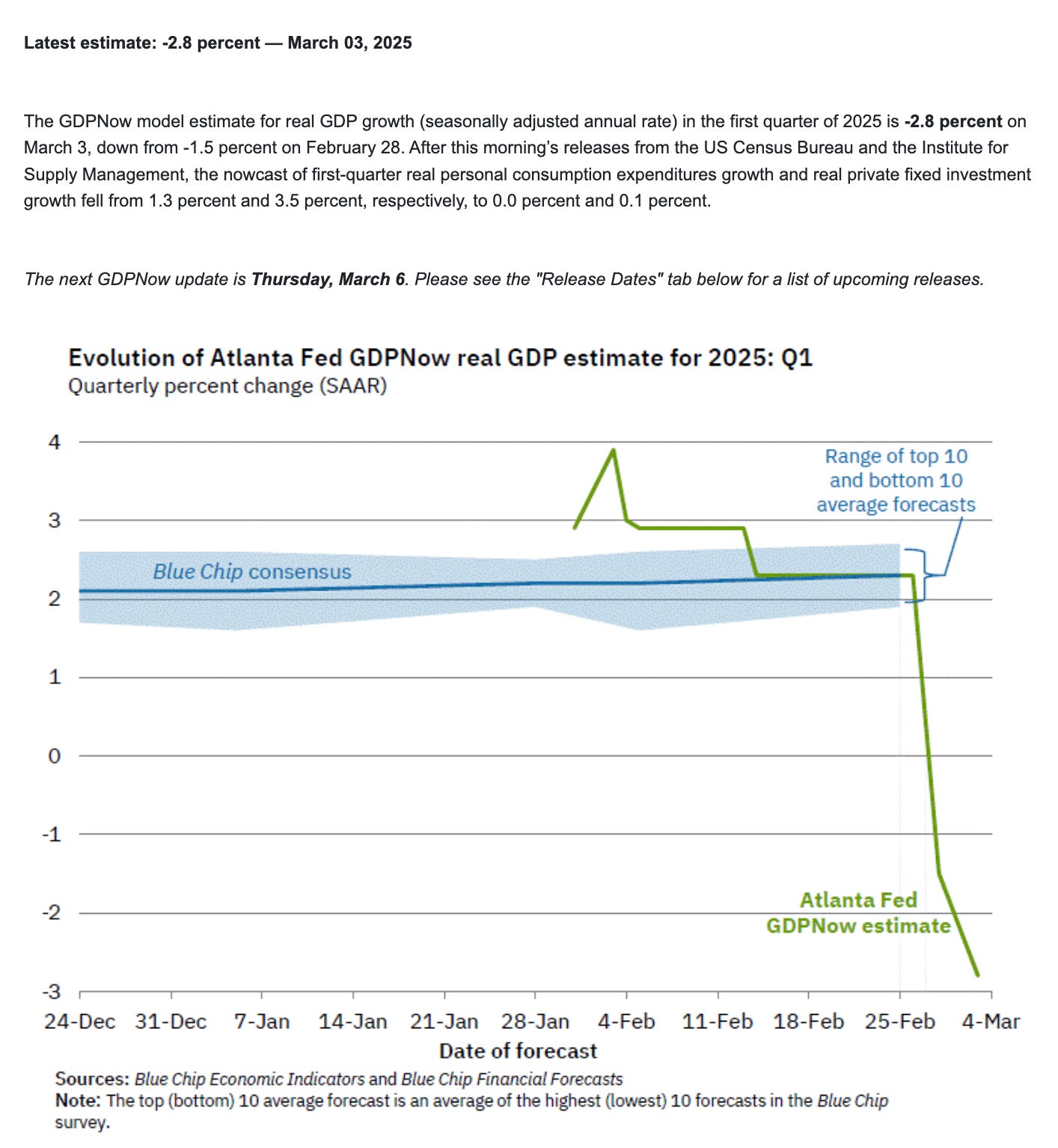

President Trump has intensified trade wars by imposing heavy tariffs on Canada, Mexico, and doubling those on China, leading these countries to retaliate. It's worth noting that during the 2018 Trade War, the market fell 20% but did not enter a bear market. Additionally, Doge's policies have resulted in higher unemployment claims in Washington D.C. and negative growth forecasts for the first quarter of 2025, according to the Atlanta Fed's real-time GDP tracking. A marked increase in imports, as importers rushed to beat the tariff deadline, has adversely impacted GDP figures, potentially priming the economy for a recession.

Investors should remember that typically, the S&P 500 falls by 5% or more at least three times annually. Currently, the index has dropped just over 5%, marking the first instance this year, with likely two more to follow. Annually, the market declines by 10% at least once, and every three years, it drops by 15% or more. Every six years, on average, the decline exceeds 20%, entering bear market territory. However, it is doubtful we will see a bear market this year; the current situation may just be a pullback or a deeper correction.

The S&P 500 will very likely post strong gains by mid-2025 due to positive market drivers but could face hurdles later in the year. Historical data by Fundstrat shows that after two consecutive years of 20% gains, markets often falter in the third year, a trend observed four out of five times since 1871. Despite consensus expectations of a down year following two robust years, markets tend to do the opposite, and is very likely to perform better than many anticipate. Reviewing past performance, the S&P 500 experienced back-to-back 20% gains during five periods: 1880, 1928, 1936, 1955, and 1996. If we look at the three-year gains that follow those leading to that 20% back-to-back, the average gain is 75%. From 2021 to 2024, the gain was only 26%. Market has not overshot compared to previous periods when markets produced these strong gains.

One example was in 1996, where the market increased by only 59% over three years, and we are currently up just 26%. By the third year, the market had risen by 31%. Based on this, 2025 US market could still conclude positively. Strong economic tailwinds, including support from the Federal Reserve and a pro-stock market president, may encourage a shift from bonds to equities. This forecast is based on historical market cycles where significant gains often followed notable declines, suggesting potential for both volatility and overall growth within the year. This healthy correction is good for tempering the market, lowering the risk of a bubble, and extending the bull market in the future. Refer back to [Are we in bubble?]

As previously discussed [All you need is patience], the VIX and KLCI indexes show a clear correlation. As detailed in my earlier article "Invest in preparedness, not in prediction" more pronounced market pullbacks and corrections typically occur as the VIX climbs, which are usually followed by very positive returns. Currently, the S&P 500 VIX has not reached a critical level like last year's August highs during the Bank of Japan's rate hike; however, the forward return remains positive. A VIX spike provides a significant investment opportunity to add more shares of quality companies using cash reserves.

Recalling the 2018 Trade War, the market initially dropped 20% and is currently down only 5%. As investors, we must be psychologically prepared for potential further declines. When the market dips, it's wise not to fully commit at once but to invest gradually, in three tranches at least, to manage the risk of deeper declines. Using reserve cash to add shares of quality companies at these times improves the portfolio fund price-to-value ratio and maintains a favorable risk-to-reward ratio. Refer back to The Best Strategy Isn't the Highest Return, But One You Can Stick With Even in Bad Times

It's fine to form opinions about the market, but as value investors, we don't base our investment decisions on these predictions. Instead, we focus on a company's fundamentals and economics. We seize opportunities to buy quality companies at reasonable prices when the market undervalues them and patiently wait when market sentiment is favorable. As last mentioned, in 2025, investors who invest in Malaysia are encouraged to concentrate on sectors driven by domestic demand to shield against global uncertainties like Trump 2.0 and geopolitical risks, among others.

Envision portfolio will take advantage on this market correction to add shares in watch list. These are my top pick:

Keep reading with a 7-day free trial

Subscribe to Envision Malaysia 10X stock investment to keep reading this post and get 7 days of free access to the full post archives.